The Growing Trend of Buy Now, Pay Later

Editor’s Note: This is a guest post written by Klarna, a global banking, payments & shopping service.

Klarna, the world’s leading global banking, payments and shopping service, recently published BNPL and the new economic landscape, an independent report by Capital Economics on the market impact, benefits and challenges of ‘Buy Now Pay Later’ for consumers and retailers.

Here are just some of the key findings.

Consumers changed the way they pay, shop and save

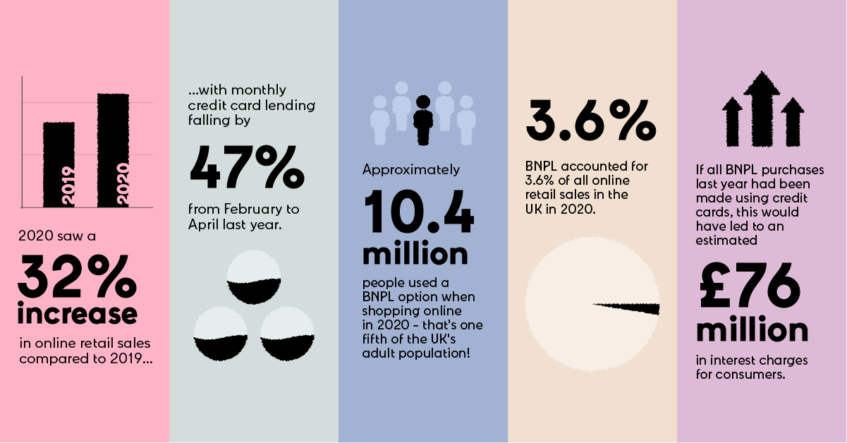

For years, consumers have been increasing how much they spend online, and this trend has only accelerated as global lockdowns made it a necessity. Online retail sales soared by 32% and, at the same time, consumers continued falling out of love with using credit cards and cash to pay and instead, opted for debit cards and digital wallets for their day-to-day purchases.

As restaurants, bars and non-essential stores were closed, consumers generally spent less. And though it was a tough year, on average, households actually tripled the amount of money they were able to put aside to £300 billion in 2020.

Of course, while consumers will be key to helping the nation’s economy bounce back, they will – understandably – be very cautious about how they spend their money. Now, more than ever, they will be looking for solutions which can give them control over their finances as well as security, flexibility and ways to avoid unnecessary costs.

The more “traditional” options don’t meet consumers’ new needs and that’s why buy now pay later (BNPL) – and Klarna – has become so popular.

In the UK, over 10 million people used BNPL services to make an online purchase in 2020. However, while BNPL is rapidly gaining in popularity, it currently represents just a small fraction of all retail sales. In 2020, UK consumers spent £4.1 billion using BNPL, just under 4% of all online purchases.

Even so, if all BNPL purchases in 2020 had been made on credit cards over the same period instead, consumers would have shelled out £76 million in interest alone, not to mention other charges like missed payment fees or membership fees. As BNPL increases its share of the market, so will the potential savings for consumers.

But what if BNPL hadn’t been an option for buying something? One third of people would have used another type of credit to make their purchases, potentially attracting not only high interest but a raft of charges. Another third would have made these purchases without using any form of credit at all, pointing to other benefits of BNPL beyond just deferring or splitting payments.

What’s so attractive about BNPL?

For consumers, BNPL benefits include security, flexibility and helping to manage finances. In fact, 78% said that the security BNPL provides when buying from unknown sellers was an important factor for their purchase decision, while 71% considered the flexibility to defer payments as important. We are also happy to see that around two thirds said that using a Pay later solution had helped them manage their finances ‘a lot’ or ‘a little’.

For retailers, BNPL offers numerous benefits including giving consumers more flexibility without taking on risks for late or non-payment. How does it work? Retailers get paid upfront from their BNPL partners every time customers make a purchase, minus a small fee. This allows customers to spread their payments with no interest charges and allows retailers to offset risks onto the BNPL provider. It’s a win-win for both!

Meet Klarna and the world of smooth

As consumer appetite for flexible payments grows, so does the market opportunity for retailers. Partnering with Klarna offers more than a BNPL service to your checkout – it is a full circle shopping destination that offers merchants the opportunity to acquire and retain customers within the Klarna ecosystem. Leverage Klarna’s channels to meet new shoppers, whether it’s through social (154m monthly impressions), the Klarna app (18m monthly average users globally), CRM, website or other owned channels and media services.