Guide to structuring your US entity and corporate tax compliance

As the world turns it back on pandemic restrictions and lockdowns, more and more businesses are not only striving to get back on their feet but also expand into newer and unchartered territories. While there are many ways to expand your business internationally, the most preferred is the direct route of incorporating your business in those countries and growing locally.

Amongst all the countries for expansion, United States stands as the #1 choice due to a multitude of reasons the main one it being the world’s biggest economy, and a stable and healthy democracy. Immigrants from all over the world have made the United States their home making it easy for others to do business there, and with English being the main language, it has become even more easy.

So, if you’re looking to expand to the US, here are the things to consider and various options available to you if you want to incorporate your business there.

Type of structure

In brief, LLC is more like a partnership company with no shares but only membership. It is a pass-through entity where all profits are taxed at the hands of the individual LLC members. But one of the main disadvantages of an LLC is that it cannot easily raise capital from investors or carry forward the profits to the next financial year, which is why this is most suitable for family enterprises, or e-commerce sellers.

INC or C-corp is the most preferred form of structure and it is treated like a private limited company with shares and shareholders who enjoy profits based on their shareholding pattern/agreement. This is an attractive structure for external investors. Most companies that are looking to raise funds in the US opt for this option. Amongst the two, a C-Corp makes better business sense from a clients’ perspective.

State of incorporation

Incorporation in the US is done on a state level; however, it’s not needed to incorporate a business in every state to do business in the US. A business can be incorporated in any state and then conduct business all over the country without any restrictions while complying with local regulations. You also do NOT have to worry about the tax part since sales tax is based on your customer state and federal tax is always at an effective rate of 21% irrespective of your state of incorporation. However, there are other important points to remember while choosing your state.

Annual maintenance fees

This should be the most important factor, as in the US every year, you have to file an annual report with the state to keep the company active. This involves paying fees that are known by many names across the states (e.g. franchisee tax, gross receipt tax, annual report fees, etc.). States like California, Nevada, Massachusetts, and Delaware have the highest minimum annual pay-out to states while New Jersey, Colorado, New York, Connecticut, Georgia, Hawaii, Michigan, Washington, and Wyoming are at the other end of the scale.

Ease of maintenance

While the minimum annual pay-out to states is a big factor, another one that is equally important is the ease of post-incorporation maintenance. Some states like Delaware, New York, Texas, and Wyoming have manual processes for amending the articles of incorporation which makes it tough and time consuming to affect changes in the articles of incorporation/organization when needed, thereby making their maintenance expensive in the medium to long run.

New Jersey/Florida/Colorado are suggested to be the best states for incorporating a business, and this allows your business to operate anywhere in the US without any restrictions.

Compliance

During incorporation, all states require to have a local registered agent and some states require you to have a business address within that state. You would also need an Employer Identification Number, also known as Federal Tax ID, before you start your business operations. Post incorporation, there are two compliances that need to be kept in mind while running a US entity. First would be corporate tax compliance (explained below) and the other would be state compliance. The state compliance is fairly simple and involves a payment of annual franchisee tax/report filing fees and reporting any changes in the company address/directors/registered agent.

US corporate tax compliance

Startups and entrepreneurs often find it challenging to prioritize tax compliance while focused on growing their companies. Between designing marketing strategies and creating a brand, they are left with little time and resources to spend on tax compliance.

If you have an incorporated entity in the US, one of the most important parts of being compliant is filing a Tax Return. The failure-to-file penalty is generally more than the failure-to-pay penalty. The penalty for filing late is normally fixed fee per month or 5 % of the unpaid taxes for each month or part of a month that a tax return is late. In case of non-payment of taxes by the tax deadline, the penalty ranges from 0.5% of 1% of unpaid taxes.

The current tax rate is 21% and it is expected to remain the same for CY 2022 too.

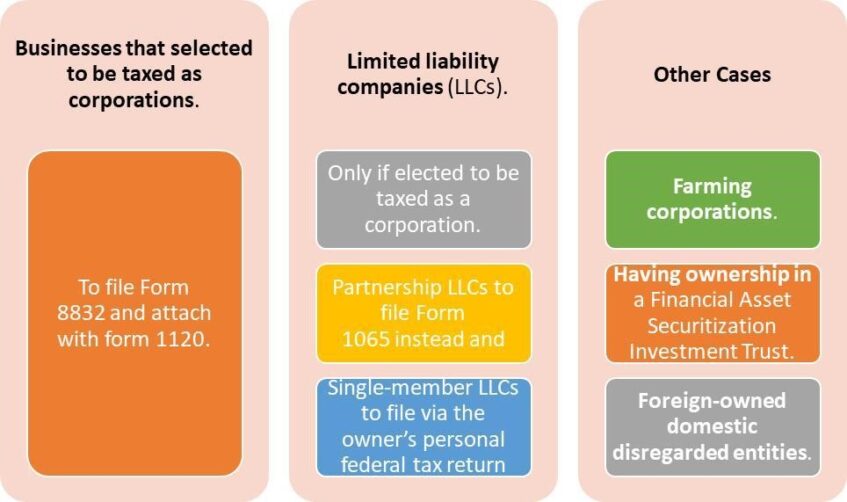

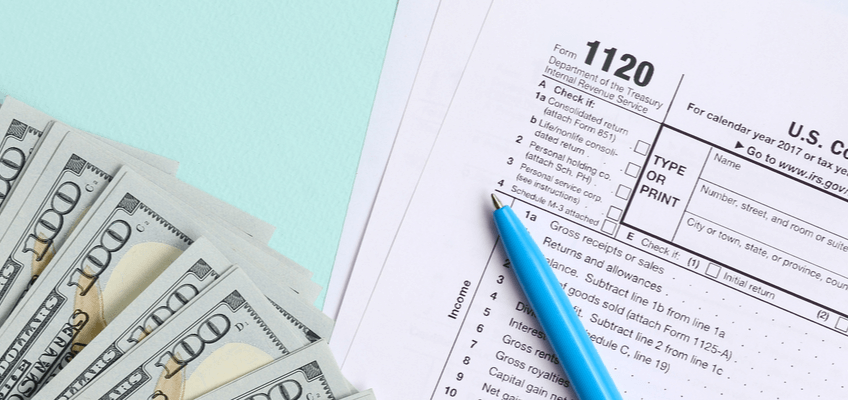

US entities file their tax return based on their structure and also if any election to the IRS is made specifically after incorporation.

C-Corporation Form 1120 – what you need to know

All domestic corporations have to file an income tax return whether or not taxable income. Domestic corporations must file Form 1120, unless they are required, or elect to file a special return. Such an entity is commonly referred to as a C Corporation and it is recognized as a separate taxpaying entity.

There are also additional documents, or schedules, that may be required to be filed along with a tax return. They include Form 1120 (Schedule N) for foreign operations of U.S. corporations and Form 1120 (Schedule D) for capital gains and losses.

✔ Who must file Form 1120

All domestic corporations must file tax form 1120, even if they don’t have taxable income. Corporations exempt under section 501 do not need to file tax Form 1120.

✔ Key Points to consider when filing Form 1120

3 important pieces of information need to be provided while filing a tax return:

- Basic information about the corporation and the return

- Various income, deductions, credits and other items necessary to determine the tax liability of the Corporation

- When applicable, Balance Sheet and reconciliation of Book Income (Loss) to the tax return

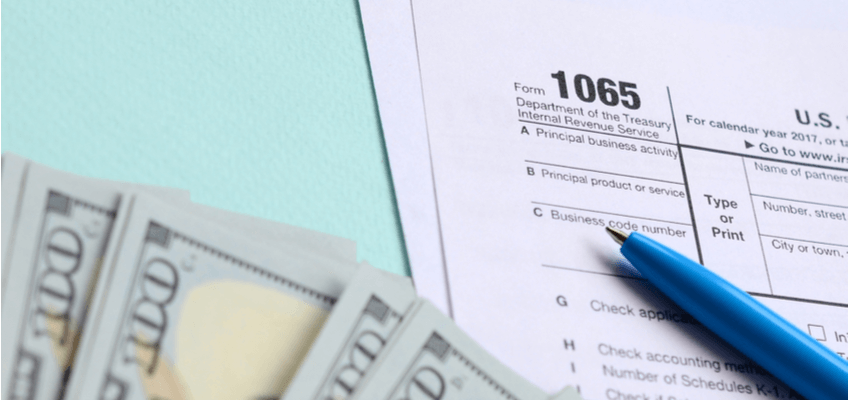

Partnerships Form 1065 – what you need to know

All domestic partnerships must file Form 1065: U.S. Return of Partnership Income. This includes limited liability corporations (LLCs) classified as domestic partnerships and headquartered in the U.S.

✔ Who must file Form 1065:

U.S. Return of Partnership Income is a tax document issued by the IRS used to declare the profits, losses, deductions, and credits of a business partnership. In addition to Form 1065, partnerships must also submit Schedule K-1, a document prepared for each partner.

Form 1065 gives the IRS a snapshot of the company’s financial status for the year. The partners must report and pay taxes on their shares of income from the partnership on their tax returns. Partners must pay income tax on their earnings regardless of whether the earnings were distributed.

✔ Key points to consider when filing Form 1065

- To declare profits, losses, deductions, and credits of a business partnership for tax filing purposes.

- This form requires significant information about the partnership’s annual financial status. This includes income information such as gross receiptsor sales, deductions and operating expenses such as rent, employee wages, bad debts, interest on business loans, and other costs. Required Information includes:

- Form 4562: Depreciation and Amortization

- Form 1125-A: Cost of Goods Sold

- Form 4797: Sale of Business Property

- Copies of any Form 1099 issued by the partnership

- Form 8918: Material Advisor Disclosure Statement

- Form 114: Report of Foreign Bank and Financial Accounts Disclosure Statement

- Form 3520: Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts

- Information about the partners and their stake in the company by percentage of ownership – to submit Schedule K-1

Opening an entity in the US can be a tricky and complicated process. The New York Business Advisory & Corporate Service (NYBACS) helps businesses looking to expand to the US incorporate their business in an efficient and compliant way so they can make the most of this exciting and lucrative market.

About NYBACS:

NYBACS (New York Business Advisory & Corporate Services Inc) offers Factoring Services and Cross-Border Payment solutions that help freelancers and exporters to receive cross-border payments from over 200 countries together onto a single platform that makes cross-border trade as easy as local trade with no upfront or signup fees. NYBACS Factoring offers funding for businesses of all sizes and stages; from start-ups to long-established companies, factoring is a smart solution to not only to combat cash flow crunches without taking on additional debt but also ensure copious liquidity for businesses.

NYBACS’s endeavors to simplify the processes, reduce the timeline, and in the end, provide an extremely affordable solutions for your business.

[1] According to eligibility and current Payoneer offering